Since July 2020, the S&P 500 has delivered a total return of 93.1%. But one standout stock has more than doubled the market - over the past five years, Booking has surged 233% to $5,702 per share. Its momentum hasn’t stopped as it’s also gained 21.7% in the last six months thanks to its solid quarterly results, beating the S&P by 17.6%.

Following the strength, is BKNG a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Are We Positive On Booking?

Formerly known as The Priceline Group, Booking Holdings (NASDAQ:BKNG) is the world’s largest online travel agency.

1. Room Nights Booked Drive Additional Growth Opportunities

As an online travel company, Booking generates revenue growth by increasing both the number of stays (or experiences) booked and the commission charged on those bookings.

Over the last two years, Booking’s room nights booked, a key performance metric for the company, increased by 9.7% annually to 319 million in the latest quarter. This growth rate is solid for a consumer internet business and indicates people are excited about its offerings.

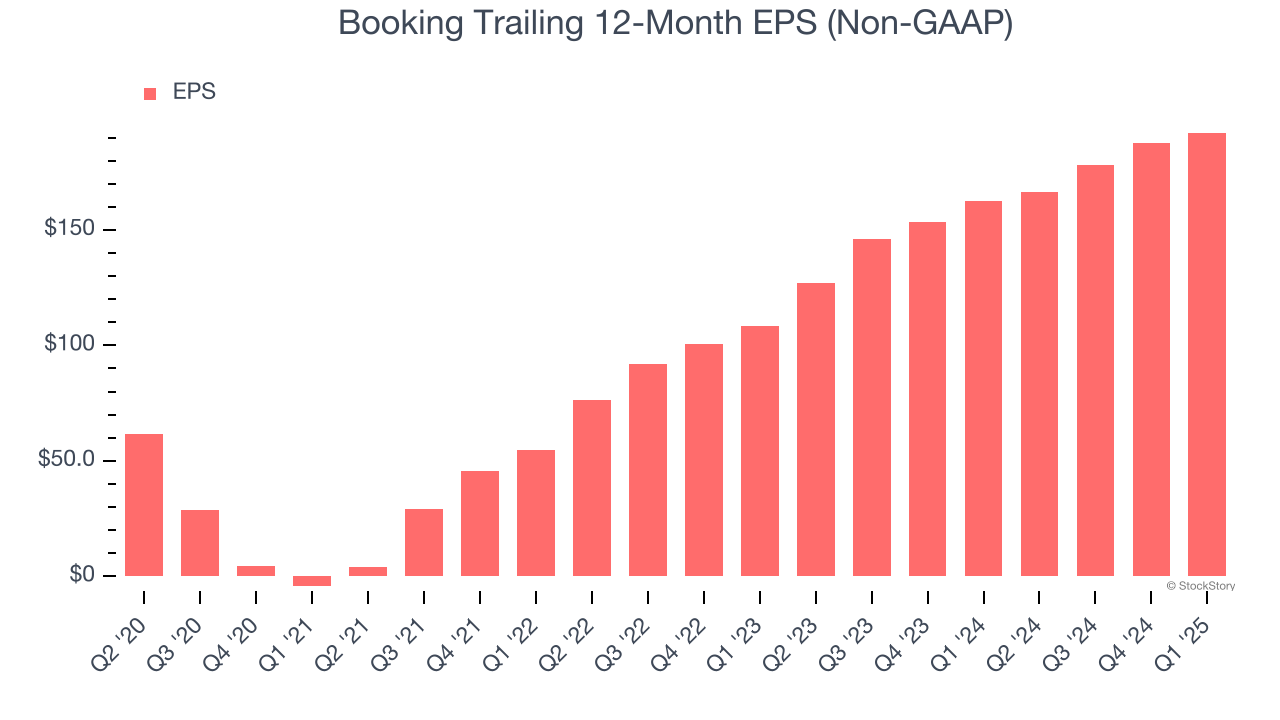

2. Outstanding Long-Term EPS Growth

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Booking’s EPS grew at an astounding 51.8% compounded annual growth rate over the last three years, higher than its 24.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

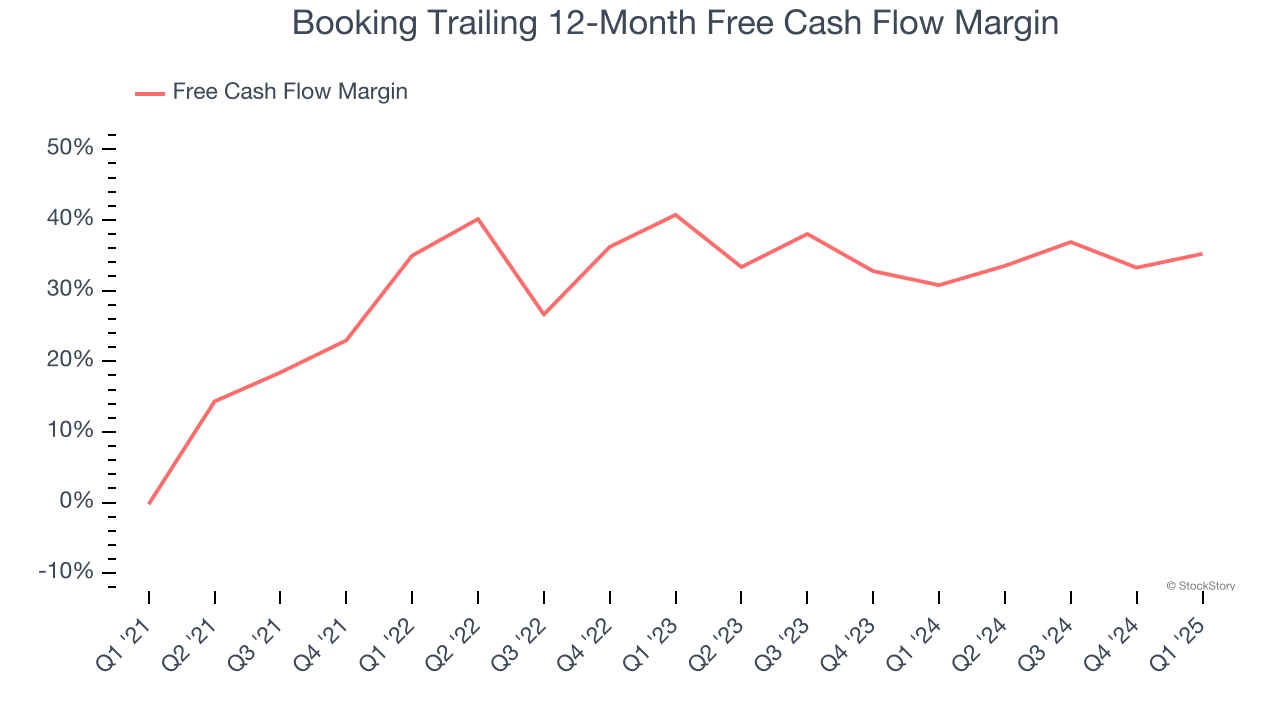

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Booking has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 33.1% over the last two years.

Final Judgment

These are just a few reasons Booking is a rock-solid business worth owning, and with its shares topping the market in recent months, the stock trades at 20.5× forward EV/EBITDA (or $5,702 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Booking

When Trump unveiled his aggressive tariff plan in April 2024, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.